Introduction

Accounts Payable is a liability on a company’s balance sheet. It represents the amount of money that a company owes to its suppliers or vendors for goods or services purchased on credit. When a company buys goods or services on credit, it incurs a liability because it has received the benefit of the goods or services but has not yet paid for them.

Accounts Payable is typically classified as a current liability, meaning it is expected to be paid off within one year. It is an essential part of the company’s working capital management, as it reflects the company’s short-term obligations to its suppliers. Managing Accounts Payable effectively is crucial for maintaining good relationships with suppliers and ensuring the smooth operation of the business.

What is an asset?

An asset is a resource with economic value that an individual, corporation, or country owns or controls with the expectation that it will provide future benefit. Assets can be tangible, such as cash, inventory, and property, or intangible, such as patents, trademarks, and goodwill.

In accounting, assets are typically classified into current assets and non-current assets. Current assets are those that are expected to be converted into cash or used up within one year, such as cash, accounts receivable, and inventory. Non-current assets, also known as long-term assets, are assets that are not expected to be converted into cash within a year, such as property, plant, and equipment.

Assets are an important part of financial analysis and are used to calculate various financial ratios, such as the current ratio and return on assets, which help assess a company’s financial health and performance.

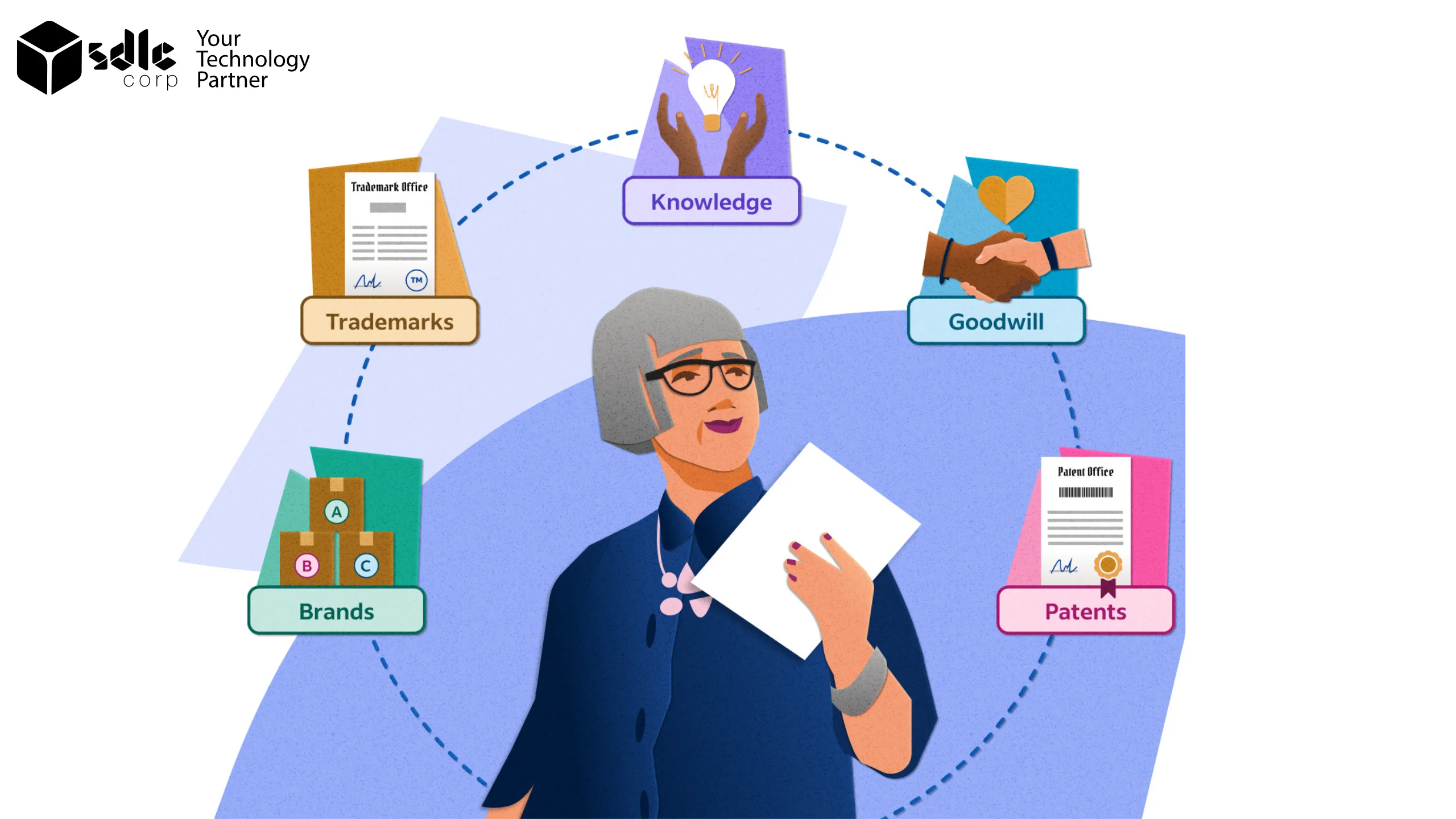

Assets are broadly classified into two categories: tangible assets and intangible assets.

- Tangible Assets: Tangible assets are physical assets that have a physical form and can be touched. Examples include cash, inventory, property, plant, and equipment. These assets are used by a company to generate revenue and are typically recorded on the balance sheet at cost less any accumulated depreciation.

- Intangible Assets: Intangible assets are assets that do not have a physical form but still have value. Examples include patents, trademarks, copyrights, goodwill, and intellectual property. Intangible assets are recorded on the balance sheet at cost less any accumulated amortization .

Learn more about managing Accounts Payable efficiently.

What is a liability?

A liability is a financial obligation or debt that an individual, business, or organization owes to another party. Liabilities can arise from borrowing money, purchasing goods or services on credit, or other obligations that require future payment or settlement. Liabilities represent claims against a company’s assets and are classified as either current or non-current on a company’s balance sheet.

- Current Liabilities: Current liabilities are obligations that are due within one year or within the normal operating cycle of the business, whichever is longer. Examples include accounts payable, wages payable, taxes payable, and short-term loans.

- Non-current Liabilities: Non-current liabilities, also known as long-term liabilities, are obligations that are due beyond one year or the normal operating cycle of the business. Examples include long-term loans, bonds payable, and lease obligations.

Liabilities are important in financial analysis as they represent the claims of creditors against a company’s assets. They are used to calculate various financial ratios, such as the debt-to-equity ratio and the current ratio, which help assess a company’s financial health and solvency. It’s important for individuals and businesses to manage their liabilities effectively to avoid financial difficulties and maintain a healthy financial position.

How do you calculate accounts payable?

To calculate accounts payable, you typically sum up all the outstanding invoices and bills that a company has yet to pay to its suppliers. Here’s a simplified formula:

Accounts Payable = Total value of outstanding invoices + Total value of outstanding bills

This calculation is straightforward for smaller businesses with fewer transactions. However, for larger companies with numerous invoices and bills, accounting software or enterprise resource planning (ERP) systems are often used to track and manage accounts payable. These systems automatically sum up the amounts owed based on the data entered for each invoice and bill.

Understand the impact of Accounts Payable on your financial statements.

Accounts payable (AP) matters for several reasons

Financial Health: AP reflects a company’s short-term financial obligations to suppliers. Managing AP effectively is crucial for maintaining good relationships with suppliers and ensuring the company’s financial health.

- Cash Flow Management: AP directly impacts cash flow. Managing AP helps in optimizing payment timing to ensure that the company has enough cash to cover its liabilities without holding excess cash that could be invested elsewhere.

- Supplier Relationships: Timely payments and effective communication with suppliers help build strong relationships. This can lead to better payment terms, discounts for early payments, and priority treatment during shortages or other issues.

- Creditworthiness: How a company manages its AP can affect its creditworthiness. Creditors and investors may look at AP levels and payment history to assess the company’s financial stability.

- Financial Reporting: Accurate and up-to-date AP records are essential for preparing financial statements and reports. This information is important for internal decision-making and for meeting regulatory requirements.

- Cost Control: Efficient AP processes can help reduce costs associated with late payments, duplicate payments, and errors in invoicing.

Overall, accounts payable is a critical aspect of financial management that impacts a company’s liquidity, profitability, and relationships with suppliers and creditors.

Accounts payable an asset or liabiity?

Accounts payable are a liability. They represent the amount of money a company owes to its suppliers or creditors for goods or services that have been received but not yet paid for. While accounts payable reflect money owed by the company, they are categorized as a liability on the balance sheet because they represent debts that must be settled in the future.

How to record debits and credits in accounts payable?

Recording debits and credits in accounts payable (AP) follows the basic principles of double-entry accounting. Here’s how it works:

- Initial Entry: When a company receives an invoice from a supplier, it records the transaction in its accounting records. The initial entry is a credit to accounts payable, increasing the amount the company owes to its suppliers.

- Payment Entry: When the company pays the invoice, it records the payment as a debit to accounts payable, reducing the amount owed, and a credit to the cash account, reducing the company’s cash balance.

- Adjustments: Sometimes, adjustments are needed in the accounts payable balance, such as for returned goods or discounts received. These adjustments are recorded as debits or credits to the accounts payable account.

- Accruals: If expenses are incurred but invoices are not yet received, the company may need to accrue for these expenses. This is done by debiting the relevant expense account and crediting accounts payable.

- Reversals: In some cases, transactions recorded in accounts receivable

may need to be reversed. For example, if an invoice is found to be incorrect and is canceled, the initial entry would be reversed by debiting accounts payable and crediting the appropriate account.

Recording debits and credits in accounts payable accurately is essential for maintaining correct financial records and ensuring that the company’s financial statements reflect its true financial position.

Explore software solutions to streamline your Accounts Payable process

FAQs

1. What are assets and liabilities?

- Assets are resources owned by a company that have economic value and can be used to generate future benefits. Examples include cash, inventory, property, and equipment.

- Liabilities are obligations that a company owes to external parties. Liabilities represent claims against a company’s assets and can include loans, accounts payable, and accrued expenses.

2. What is the difference between assets and liabilities?

The main difference is that assets represent what a company owns and can use to generate future income, while liabilities represent what a company owes to others. Assets are recorded on the left side (debit) of the balance sheet, while liabilities are recorded on the right side (credit).

3. How are assets and liabilities related to the balance sheet?d for different businesses?

The balance sheet is a financial statement that provides a snapshot of a company’s financial position at a specific point in time. It lists the company’s assets, liabilities, and shareholders’ equity. The balance sheet equation is Assets = Liabilities + Shareholders’ Equity.

4. How are assets and liabilities categorised?

Assets are typically categorised as current assets (expected to be converted to cash within one year) or non-current assets (long-term assets like property and equipment). Liabilities are categorised as current liabilities (due within one year) or non-current liabilities (long-term obligations like loans).

5. How do assets and liabilities impact financial analysis?

Assets and liabilities are key components in financial analysis. They are used to calculate important ratios such as the current ratio (current assets divided by current liabilities), which measures a company’s ability to cover its short-term obligations. They also help assess a company’s liquidity, solvency, and overall financial health.

Contact Us

Share a few details about your project, and we’ll get back to you soon.

Let's Talk About Your Project

- Free Consultation

- 24/7 Experts Support

- On-Time Delivery

- sales@sdlccorp.com

- +1(510-630-6507)